Tutorial¶

Contents:

Getting Started¶

To get started, install the library with pip

pip install anticipy

It is straightforward to generate a forecast with the tool -

just call forecast.run_forecast(my_dataframe)():

import pandas as pd, numpy as np

from anticipy import forecast, forecast_models, forecast_plot

df = pd.DataFrame({'y': np.full(20,10.0)+np.random.normal(0.0, 0.1, 20),

'date':pd.date_range('2018-01-01', periods=20, freq='D')})

df_forecast = forecast.run_forecast(df, extrapolate_years=0.5)

print(df_forecast.tail(3))

Output:

. date source is_actuals model y q5 q20 q80 q95

219 2018-07-19 src False linear 9.490259 7.796581 8.339835 10.556202 11.689470

220 2018-07-20 src False linear 9.487518 7.828049 8.362620 10.466285 11.640854

221 2018-07-21 src False linear 9.484776 7.776001 8.343068 10.423964 11.696145

The tool automatically selects the best model from a list of defaults - in this case, a simple linear model. Advanced users can instead provide their preferred model or lists of candidate models, as explained in Forecast models.

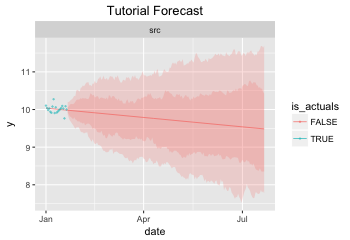

You can plot the forecast output using the functions in forecast_plot.

anticipy.forecast_plot.plot_forecast() saves the plot as a file or

exports it to a jupyter notebook. The plot looks as follows:

The code to generate the plot is:

path_tutorial_plot = 'plot-tutorial'

# Save plot as a file

forecast_plot.plot_forecast(df_forecast, output='html',

path=path_tutorial_plot, width=350, height=240, title='Tutorial Forecast')

# Show plot in a jupyter notebook

forecast_plot.plot_forecast(df_forecast, output='jupyter', width=350,

height=240, title='Tutorial Forecast')

Input Format¶

The input time series needs to be formatted as a pandas series or dataframe. If a dataframe is passed, the following columns are used:

y: float, values of the time series.

date: (optional) timestamp, date and time of each sample. If this column is not present, and the dataframe index is a DatetimeIndex, the index will be used instead. This is an optional column, only required when using models that are aware of the date, such as weekly seasonality models.

x: (optional) float or int, numeric index of each sample. If this column is not present, it will be inferred from the date column or, if that is not possible, the dataframe index will be used instead.

source: (optional) string, the name of the data source for this time series. You can include multiple time series in your input dataframe, using different source values to identify them.

If a series is passed, ‘y’ will be the series values and, if the index is a DateTimeIndex, it will be used as the ‘date’ column. If the index is numeric, it will be used as the ‘x’ column instead.

An input dataframe should meet the following constraints:

Minimum required samples depends on number of parameters in the chosen models. run_forecast() will fail to fit if n_samples < n_parameters+2

y column may include null values.

Multiple values per sample may be included, e.g. when the same metric is observed by multiple sources. In that case, it is possible to assign weights to each individual sample so that one source will be given higher priority. To do that, include a ‘weight’ column of floats in the input dataframe.

A date column or date index is only required if the model is date-aware.

Non-default column names may be used. In that case, you need to pass the new column names to run_forecast() using the col_name_ parameters.

Here is an example of using col_name_ parameters to run a forecast witn non-default column names:

df2 = pd.DataFrame({'my_y': np.full(20,10.0)+np.random.normal(0.0, 0.1, 20),

'my_date':pd.date_range('2018-01-01', periods=20, freq='D')})

df_forecast2 = forecast.run_forecast(df2, extrapolate_years=0.5,

col_name_y='my_y',

col_name_date='my_date')

Detailed Output¶

The library uses scipy.optimize to fit model functions to the input data. You can examine the model parameters, quality metrics and other useful information with the argument simplify_output=False:

dict_result = forecast.run_forecast(df, extrapolate_years=0.5,

simplify_output=False, include_all_fits=True)

# Table with actuals and forecast for best-fitting model, including prediction intervals

print dict_result['forecast'].groupby('model').tail(1)

# Table including time series actuals and forecast

print dict_result['data'].groupby('model').tail(1)

# Metadata table: model parameters and fitting output

print dict_result['metadata']

# Table with output data from scipy.optimize, for debugging purposes

print dict_result['optimize_info']

Output - forecast table, same as output from run_forecast(simplify_output=True):

. date source is_actuals model y q5 q20 q80 q95

19 2018-01-20 src True y 9.928176 NaN NaN NaN NaN

221 2018-07-21 src False (linear+ramp) 10.838865 9.597208 10.121438 11.717812 12.551523

Output - data table. Has actuals and forecasts, including forecasts from non-optimal models if include_all_fits=True

. date model y source source_long is_actuals is_weight is_filtered is_best_fit

19 2018-01-20 weight 1.000000 src src:1-1:D:2018-01-01::2018-01-20 True True False False

39 2018-01-20 y 9.928176 src src:1-1:D:2018-01-01::2018-01-20 True False False False

241 2018-07-21 linear 9.230972 src src:1-1:D:2018-01-01::2018-01-20 False False False False

443 2018-07-21 (linear+season_wday) 9.283372 src src:1-1:D:2018-01-01::2018-01-20 False False False False

645 2018-07-21 (linear+ramp) 10.838865 src src:1-1:D:2018-01-01::2018-01-20 False False False True

847 2018-07-21 ((linear+ramp)+season_wday) 10.989835 src src:1-1:D:2018-01-01::2018-01-20 False False False False

Output - metadata table. Includes model parameters and model quality metrics such as cost and AICC:

. source model weights actuals_x_range freq is_fit cost aic_c params_str status source_long params is_best_fit

0 src linear 1-1 2018-01-01::2018-01-20 D True 0.063076 -111.182993 [-3.9e-03 1.0e+01] FIT src:1-1:D:2018-01-01::2018-01-20 [-0.0038931365581278176, 10.013491979601325] False

1 src (linear+season_wday) 1-1 2018-01-01::2018-01-20 D True 0.039519 -95.533948 [-3.3e-03 1.0e+01 1.0e-01 -1.4e-02 8.4e-02 ... FIT src:1-1:D:2018-01-01::2018-01-20 [-0.0032764198059819344, 9.975993454168774, 0.... False

2 src (linear+ramp) 1-1 2018-01-01::2018-01-20 D True 0.045997 -111.498115 [-0. 10.1 6. 0. ] FIT src:1-1:D:2018-01-01::2018-01-20 [-0.030005422538483477, 10.103677325164737, 6.... True

3 src ((linear+ramp)+season_wday) 1-1 2018-01-01::2018-01-20 D True 0.020303 -93.853970 [-3.2e-02 1.0e+01 6.0e+00 3.8e-02 1.1e-01 ... FIT src:1-1:D:2018-01-01::2018-01-20 [-0.0318590092714045, 10.062880686158646, 6.00... False

Output - optimize information table. Includes detailed data generated by scipy.optimize, useful for debugging:

. source model success params_str cost optimality iterations status jac_evals message source_long params

0 src linear True [-3.9e-03 1.0e+01] 0.063076 1.213028e-09 4 1 4 `gtol` termination condition is satisfied. src:1-1:D:2018-01-01::2018-01-20 [-0.0038931365581278176, 10.013491979601325]

1 src (linear+season_wday) True [-3.3e-03 1.0e+01 1.0e-01 -1.4e-02 8.4e-02 ... 0.039519 8.348877e-14 4 1 4 `gtol` termination condition is satisfied. src:1-1:D:2018-01-01::2018-01-20 [-0.0032764198059819344, 9.975993454168774, 0....

2 src (linear+ramp) True [-0. 10.1 6. 0. ] 0.045997 1.765921e-03 34 2 22 `ftol` termination condition is satisfied. src:1-1:D:2018-01-01::2018-01-20 [-0.030005422538483477, 10.103677325164737, 6....

3 src ((linear+ramp)+season_wday) True [-3.2e-02 1.0e+01 6.0e+00 3.8e-02 1.1e-01 ... 0.020303 2.777755e-02 45 2 28 `ftol` termination condition is satisfied. src:1-1:D:2018-01-01::2018-01-20 [-0.0318590092714045, 10.062880686158646, 6.00...

Forecast models¶

By default, run_forecast() automatically generates a list of candidate models. However, you can specify a list of models in the argument l_model_trend, so that the tool fits each model and chooses the best. Only the best fitting model will be included in the output, unless you use the argument include_all_fits=True. The following example runs a forecast with two models: linear and constant:

dict_result = forecast.run_forecast(df, extrapolate_years=1, simplify_output=False,

l_model_trend = [forecast_models.model_linear,

forecast_models.model_constant],

include_all_fits=True)

# Table including time series actuals and forecast

print dict_result['data'].tail(6)

# Metadata table: model parameters and fitting output

print dict_result['metadata']

Output:

. date model y source source_long is_actuals is_weight is_filtered is_best_fit

739 2018-12-31 constant 2.0 src src:1:D:2018-01-01::2018-01-05 False False False False

740 2019-01-01 constant 2.0 src src:1:D:2018-01-01::2018-01-05 False False False False

741 2019-01-02 constant 2.0 src src:1:D:2018-01-01::2018-01-05 False False False False

742 2019-01-03 constant 2.0 src src:1:D:2018-01-01::2018-01-05 False False False False

743 2019-01-04 constant 2.0 src src:1:D:2018-01-01::2018-01-05 False False False False

744 2019-01-05 constant 2.0 src src:1:D:2018-01-01::2018-01-05 False False False False

. source model weights actuals_x_range freq is_fit cost aic_c params_str status source_long params is_best_fit

0 src linear 1 2018-01-01::2018-01-05 D True 6.162976e-33 -368.880931 [1.0e+00 1.1e-16] FIT src:1:D:2018-01-01::2018-01-05 [1.0, 1.1102230246251565e-16] True

1 src constant 1 2018-01-01::2018-01-05 D True 5.000000e+00 3.000000 [2.] FIT src:1:D:2018-01-01::2018-01-05 [2.0] False

You can configure run_forecast to fit a seasonality model in addition to the trend model. To do so, include the argument l_model_season with a list of one or more seasonality models. If the list includes model_null, a non-seasonal model will also be fit and compared with the seasonal models. The function tries all combinations of trend models and seasonality models and selects the best:

df=pd.DataFrame({'y': np.full(21, 10.)+np.tile(np.arange(0., 7),3)},

index=pd.date_range('2018-01-01', periods=21, freq='D'))

dict_result = forecast.run_forecast(df, extrapolate_years=0.5, simplify_output=False,

l_model_trend = [forecast_models.model_linear,

forecast_models.model_constant],

l_model_season = [forecast_models.model_null, # no seasonality model

forecast_models.model_season_wday], # weekday seasonality model

include_all_fits=True)

print dict_result['data'].tail(6)

print dict_result['metadata'][['source','model','is_fit','cost','aic_c','params_str','is_best_fit']]

Output:

. date model y source source_long is_actuals is_weight is_filtered is_best_fit

2331 2019-01-16 (constant_mult_season_wday) 12.0 src src:1:D:2018-01-01::2018-01-21 False False False False

2332 2019-01-17 (constant_mult_season_wday) 13.0 src src:1:D:2018-01-01::2018-01-21 False False False False

2333 2019-01-18 (constant_mult_season_wday) 14.0 src src:1:D:2018-01-01::2018-01-21 False False False False

2334 2019-01-19 (constant_mult_season_wday) 15.0 src src:1:D:2018-01-01::2018-01-21 False False False False

2335 2019-01-20 (constant_mult_season_wday) 16.0 src src:1:D:2018-01-01::2018-01-21 False False False False

2336 2019-01-21 (constant_mult_season_wday) 10.0 src src:1:D:2018-01-01::2018-01-21 False False False False

. source model is_fit cost aic_c params_str is_best_fit

0 src linear True 3.741818e+01 16.130320 [ 0.1 11.9] False

1 src (linear_add_season_wday) True 1.840127e-15 -742.442745 [3.5e-10 6.3e+00 3.7e+00 4.7e+00 5.7e+00 6.7e+... False

2 src constant True 4.200000e+01 16.556091 [13.] False

3 src (constant_add_season_wday) True 1.686607e-15 -750.272181 [12.7 -2.7 -1.7 -0.7 0.3 1.3 2.3 3.3] False

4 src (linear_mult_season_wday) True 2.761458e-16 -782.272627 [-2.2e-10 1.9e+01 5.3e-01 5.9e-01 6.4e-01 ... True

5 src (constant_mult_season_wday) True 6.833738e-13 -624.181393 [15.9 0.6 0.7 0.8 0.8 0.9 0.9 1. ] False

The following trend and seasonality models are currently supported. They are available as attributes from

anticipy.forecast_models:

name |

params |

formula |

notes |

|---|---|---|---|

model_null |

0 |

y=0 |

Does nothing. Used to disable components (e.g. seasonality) |

model_linear |

2 |

y=Ax + B |

Linear model |

model_ramp |

2 |

y = (x-A)*B if x>A |

Ramp model |

model_season_wday |

6 |

see desc. |

Weekday seasonality model. Assigns a constant value to each weekday |

model_season_fourier_yearly |

20 |

see desc |

Fourier yearly seasonality model |

name |

params |

formula |

notes |

|---|---|---|---|

model_constant |

1 |

y=A |

Constant model |

model_linear_nondec |

2 |

y=Ax + B |

Non decreasing linear model. With boundaries to ensure model slope >=0 |

model_quasilinear |

3 |

y=A*(x^B) + C |

Quasilinear model |

model_exp |

2 |

y=A * B^x |

Exponential model |

model_decay |

4 |

Y = A * e^(B*(x-C)) + D |

Exponential decay model |

model_step |

2 |

y=0 if x<A, y=B if x>=A |

Step model |

model_two_steps |

4 |

see model_step |

2 step models. Parameter initialization is aware of # of steps. |

model_sigmoid_step |

3 |

y = A + (B - A) / (1 + np.exp(- D * (x - C))) |

Sigmoid step model |

model_sigmoid |

3 |

y = A + (B - A) / (1 + np.exp(- D * (x - C))) |

Sigmoid model |

model_season_wday_2 |

2 |

see desc. |

Weekend seasonality model. Assigns a constant to each of weekday/weekend |

model_season_month |

11 |

see desc. |

Month seasonality model. Assigns a constant value to each month |

If the available range of models isn’t a good match for your data, it is also possible to define new models

using anticipy.forecast_models.ForecastModel

Models with dummy variables¶

You can use anticipy.forecast_models.get_model_dummy() to get a model based on a dummy variable. This

model returns a constant value when the dummy variable is 1, and 0 otherwise:

# Example dummy model - check if date matches specific dates in list

model_dummy_l_date = forecast_models.get_model_dummy('dummy_l_date', ['2017-12-22', '2017-12-27'])

# Example dummy model - checks if it is Christmas

model_dummy_christmas = forecast_models.get_model_dummy('dummy_christmas',

lambda a_x, a_date: ((a_date.month == 12) & (a_date.day == 25)).astype(float))

a_x = np.arange(0,10)

a_date = pd.date_range('2017-12-21','2017-12-30')

params = np.array([10.]) # A=10

print model_dummy_l_date(a_x, a_date, params)

print model_dummy_christmas(a_x, a_date, params)

Output:

[ 0. 10. 0. 0. 0. 0. 10. 0. 0. 0.]

[ 0. 0. 0. 0. 10. 0. 0. 0. 0. 0.]

Dummy variables can be very useful when used in composition with simpler models. A common application is to check for bank holidays or other special dates. The following example uses a dummy variable to improve fit in a linear time series with a spike on Christmas:

df=pd.DataFrame({'y': 100+np.arange(0,6)+np.array([0.,0.,0.,0.,50.,0.,])},

index=pd.date_range('2017-12-21','2017-12-26'))

# Example dummy model - checks if it is Christmas

model_dummy_christmas = forecast_models.get_model_dummy('dummy_christmas',

lambda a_x, a_date: ((a_date.month == 12) & (a_date.day == 25)).astype(float))

dict_result = forecast.run_forecast(df, extrapolate_years=1, simplify_output=False,

l_model_trend = [forecast_models.model_linear,

forecast_models.model_linear+model_dummy_christmas],

include_all_fits=True)

print dict_result['metadata'][['source','model','is_fit','cost','aic_c','params_str','is_best_fit']]

Output:

. source model is_fit cost aic_c params_str is_best_fit

0 src linear True 8.809524e+02 37.935465 [ 5.3 97.6] False

1 src (linear_add_dummy_christmas) True 9.980807e-20 -255.256784 [ 1. 100. 50.] True

Outlier Detection¶

If you call anticipy.forecast.run_forecast() and specify as input find_outliers=True,

it will try to automatically identify any outliers exist in the input Series. The weight for these samples is

set to 0, so that they are ignored by the forecast logic.

Example:

a_y = [19.8, 19.9, 20.0, 20.1, 20.2, 20.3, 20.4, 20.5,

20.6, 10., 20.7, 20.8, 20.9, 21.0,

21.1, 21.2, 21.3, 21.4, 21.5]

a_date = pd.date_range(start='2018-01-01', periods=len(a_y), freq='D')

df_spike = pd.DataFrame({'y': a_y})

dict_result = forecast.run_forecast(df_spike, find_outliers=True,

simplify_output=False, include_all_fits=True,

season_add_mult='add')

df_data = dict_result['data']

# Subset of output - shows that the sample with a spike now has weight=0, and is ignored by forecast

df_weighted_actuals = df_data.loc[df_data.model=='actuals'][['y','weight']]

Output:

. y weight

0 19.8 1.0

1 19.9 1.0

2 20.0 1.0

3 20.1 1.0

4 20.2 1.0

5 20.3 1.0

6 20.4 1.0

7 20.5 1.0

8 20.6 1.0

9 10.0 0.0

10 20.7 1.0

11 20.8 1.0

12 20.9 1.0

13 21.0 1.0

14 21.1 1.0

15 21.2 1.0

16 21.3 1.0

17 21.4 1.0

18 21.5 1.0